FICO, FICO, FICO…is it really all about keeping score? When we think of credit scores, or the most popular FICO score our thoughts probably pop to acquiring a loan with the higher score “scoring” the lowest credit rates. That is the elementary definition but what exactly does our FICO score tell lenders, what does it tell us??? I will share with you the common knowledge of FICO scores in layman’s terms and my experience with them, the good, the bad and the ugly, over the years. My intent here is not to reinvent the wheel so I have included several links throughout the article for more in-depth analysis of each FICO credit score criteria.

- Of course the #1 criteria that goes into your FICO score is: Payment History (35%). I say of course because as the old saying goes “those who do not learn from history, are doomed to repeat it”. Lenders do not want to star in your one man unworthy of good credit show. With that being said, let’s focus on the positive. Your payment history is derived from many different types of loans: mortgage loans; credit cards; retail/store credit cards; car loans and finance company loans. With such an array of credit going into the pot there is definitely lots to work with in terms of creating and maintaining a positive history. WMR is here to tell you from their experience that if a payment is due on the 1st but isn’t received until the 2nd, 3rd or 4th on occasion, your FICO score will not automatically drop.

- Criteria #2-Amounts Owed (30%). In as layman’s terms as I can get, if you carry high balances on your revolving credit-Visa, Amex, Mastercard, Sears, Macy’s, Petco (not even sure if they have one, but you get the point) your score can be very negatively impacted. Why say you??? Because it looks like you have overextended or may possibly overextend yourself in the future. Even with installment loans, which are usually backed by some sort of collateral such as a home or car, if you aren’t that far into your payment schedule it can impact your credit score a few points here or there. WMR is here to tell you from their experience even if you pay your credit card off in full every month depending on when your score is pulled it might still show you have a balance because your last statement balance is usually what is reported to the credit bureaus.

- Criteria #3-Length of Credit History (15%). I have not provided a link to this topic because it is pretty clear cut. This is just part of the score that simply comes with history. If you have a short history, but have managed your credit well your scores will most probably reflect your good decisions. On the contrary if you have managed credit for a long time but have done so not so good shall we say, this criteria might not help your score. WMR is here to tell you from their experience this criteria is only 15%, moving on.

- Criteria #4-What’s in your Credit Mix (10%). Getting down to the nitty-gritty, yeah only 10% does this criteria represent. It is often a good indicator of good credit worthiness if you have both revolving and installment type loans in your portfolio. HOWEVER, is not always necessary. This is one of those crazy criteria, IMHO, because it depends on many factors that come from your credit report and isn’t very quantifiable for the layman. WMR is here to tell you from their experience don’t stress too much on this criteria, just be mindful.

- Criteria #5-New Credit (10%). It just isn’t wise to open too many revolving accounts at once, if you are new in the credit game. On the other hand, WMR is here to tell you from their experience sometimes that isn’t so detrimental to your overall score if you have been managing credit for a good bit of time, 1-5 years or more.

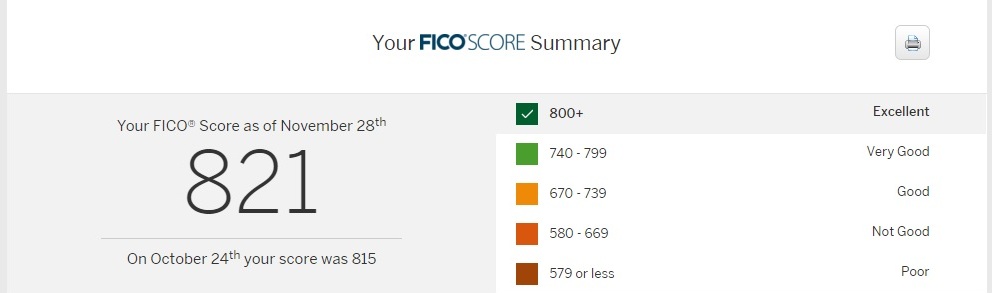

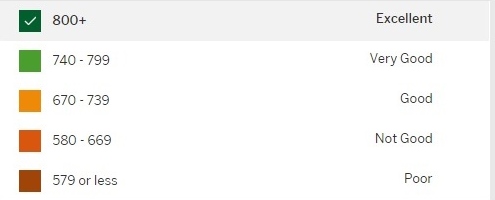

Synopsis: A FICO or any other credit score is just a numerical snapshot of your overall credit history. It helps lenders pull everything together into a quantifiable method to determine credit worthiness in an efficient manner to either extend credit to you or not extend it to you and determine the rates you will pay for their lending you money. Credit Scores are a fluid, living organism, if you will. They will go up, they will go down. Always remember you are more than just a “number” but that “number” will be with you for the duration of your financial life, treat it with respect and all that goes into it and it will repay in kind with lower interest rates! 🙂

I encourage you to leave a comment or a success experience you have had!! The Leave a Reply fields are optional, if you want to remain anonymous just fill in the comment section and hit post! Thank you for sharing your experiences and remember “no [wo]man is an island.”

Kimberly

Latest posts by Kimberly (see all)

- No Spend January - January 1, 2025

- Hot Artichoke Dip with Crostini - January 1, 2025

- Reduce Holiday Debt While Simultaneously Saving Money (Even A Little Bit Counts) - January 1, 2025